Private up, HDB down: what the Q2 2026 flash estimates really show

![]() By Alvin Ang

By Alvin Ang

Singapore’s two housing markets just moved in opposite directions. Private home prices rose 0.5% in the second quarter while HDB resale prices slipped 0.3%, the first back-to-back quarterly decline in nearly seven years. The details matter more than the headline, especially if you own a flat and plan to upgrade.

What the numbers say

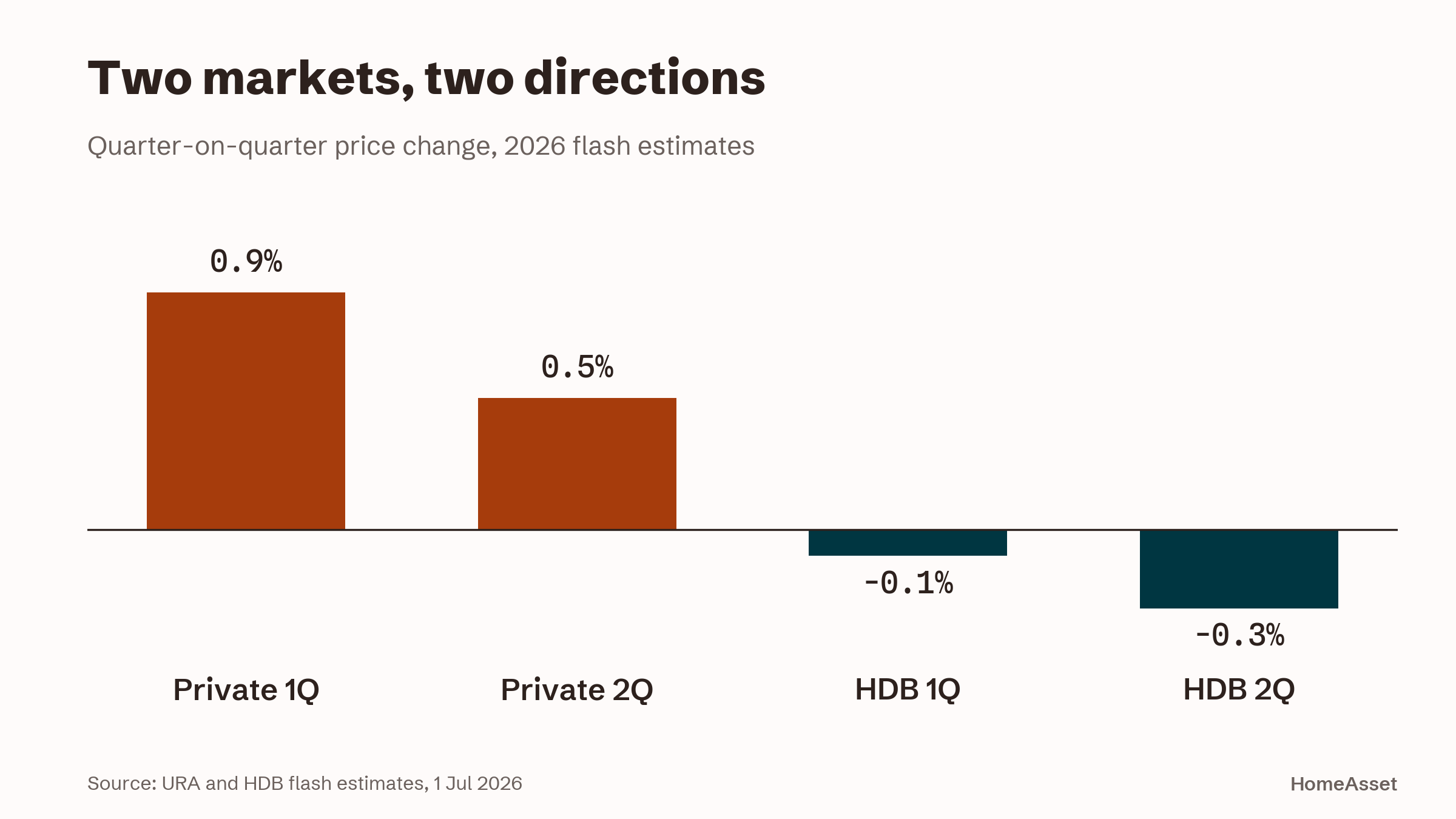

URA’s flash estimate, released on 1 July, puts overall private residential prices up 0.5% quarter-on-quarter in Q2 2026, slower than the 0.9% rise in Q1. Sale volumes were essentially flat: 5,420 transactions counted up to mid-June, against 5,413 in the first quarter.

Private prices kept rising in 2026 while HDB resale prices slipped for two straight quarters. Chart: HomeAsset. Data: URA and HDB flash estimates, 1 Jul 2026

Private prices kept rising in 2026 while HDB resale prices slipped for two straight quarters. Chart: HomeAsset. Data: URA and HDB flash estimates, 1 Jul 2026

HDB’s flash estimate tells the opposite story. The Resale Price Index eased 0.3% to 202.7, following a 0.1% dip in Q1. ERA Singapore notes this is the first time HDB resale prices have softened for two consecutive quarters since the stretch from 3Q 2018 to 2Q 2019. Resale volume held steady at 6,268 flats, from 6,285 the quarter before, though the half-year total of 12,553 sits 8.3% below the same period last year.

To put the drift in perspective: a 0.3% move on a $600,000 flat is about $1,800. This is a market losing altitude gently, not one falling.

The private rise is not what it looks like

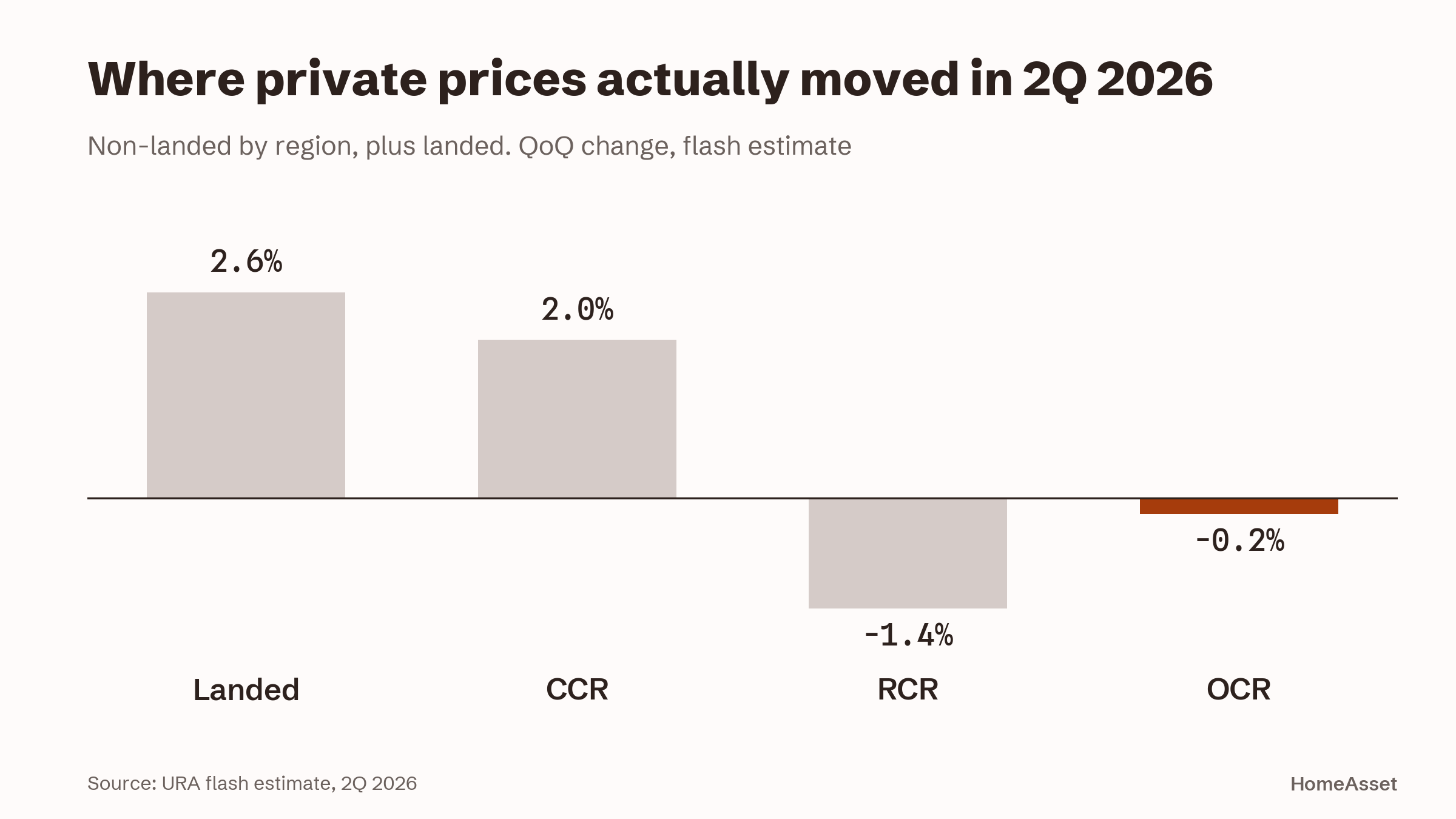

The 0.5% headline rise came from landed homes and the prime districts. City-fringe and mass-market prices fell. Data: URA flash estimate, 2Q 2026.

The 0.5% headline rise came from landed homes and the prime districts. City-fringe and mass-market prices fell. Data: URA flash estimate, 2Q 2026.

Split the private index open and the 0.5% gain disappears for most buyers. Landed homes jumped 2.6% and non-landed prices in the Core Central Region, the prime districts, rose 2.0%. Everywhere else softened: city-fringe (Rest of Central Region) prices dropped 1.4%, and mass-market (Outside Central Region) prices slipped 0.2% after rising 2.2% the quarter before.

In other words, the condos most HDB upgraders actually buy got very slightly cheaper this quarter. The index rose on the back of landed property and the prime districts, two segments most buyers are not shopping in.

Why HDB resale is cooling

ERA’s key executive officer Eugene Lim reads the softening as housing policy doing its job rather than buying sentiment breaking down. The 15-month wait-out period for private-property sellers and a larger BTO pipeline have been easing pressure on resale prices since 2025, and he sees a longer stretch of price stability as possible, while calling it too early to describe this as a correction.

Supply is the bigger force at work. ERA highlights that 13,480 flats reach their five-year minimum occupation period (MOP) in 2026, almost double the 6,973 units in 2025. These young resale flats, with more than 90 years of lease remaining, are direct competition for anyone selling an older flat, especially in Toa Payoh and Queenstown, which lead this year’s MOP supply.

Million-dollar flats keep making headlines, and the numbers are real: 491 deals in Q2 and 902 in the first half of 2026, ahead of the 763 recorded a year earlier. Keep them in proportion. They made up about 7.9% of the quarter’s resale transactions, while roughly 71% of flats still changed hands below $750,000.

More supply is coming, on both sides

URA used the same release to underline the pipeline: 4,745 private homes will be launched on the Confirmed List in the second half of 2026, taking the full year to 9,320 units, more than 50% above the past decade’s annual average. Around 61,000 private homes, including executive condominiums, are expected to complete over the next few years. On the public side, ERA points to October’s BTO exercise as the year’s largest, with 7,970 flats on offer including projects at Toa Payoh West and Bayshore.

URA’s release also carried an unusually direct note of caution: with the macroeconomic outlook highly uncertain, households are advised to exercise prudence when buying property and taking out mortgage loans.

What this means for you

- Upgrading from a flat to a mass-market condo? The maths barely changed this quarter: your flat drifted down about 0.3% while the condos you are shopping for eased 0.2%. The bigger risk to your plan is competition from newly MOP-ed flats in your own town when you sell, not the headline index.

- Buying? Softer prices with steady volumes mean more negotiating room than most quarters since 2024, and the heavy supply pipeline is an argument against fear-of-missing-out pricing.

- Selling a city-fringe or suburban condo? Momentum has cooled. Benchmark against the last three months of transactions in your project, not against last year’s highs.

- These are flash numbers compiled up to mid-June. URA publishes its full Q2 statistics on 24 July, and flash figures do get revised. For the full year, ERA still expects HDB resale prices to finish 2026 higher by 2% to 5%.

Sources

Market commentary dated 5 July 2026. Conditions change; verify figures against the primary sources above before acting. This is general information, not financial advice.