People's Park Centre tries en bloc again, $320m below 2022's ask

![]() By Alvin Ang

By Alvin Ang

People’s Park Centre, the Chinatown landmark built on the very first plot ever sold under the Government Land Sales programme in 1967, has launched its third attempt at a collective sale. The guide price of $1.48 billion is $320 million below the 2022 ask, and the tender runs from 16 July to 16 September 2026.

The owners cleared the key legal hurdle with 80.54% of the building’s share value signed on, above the 80% threshold a collective sale needs. ERA Realty is marketing the tender.

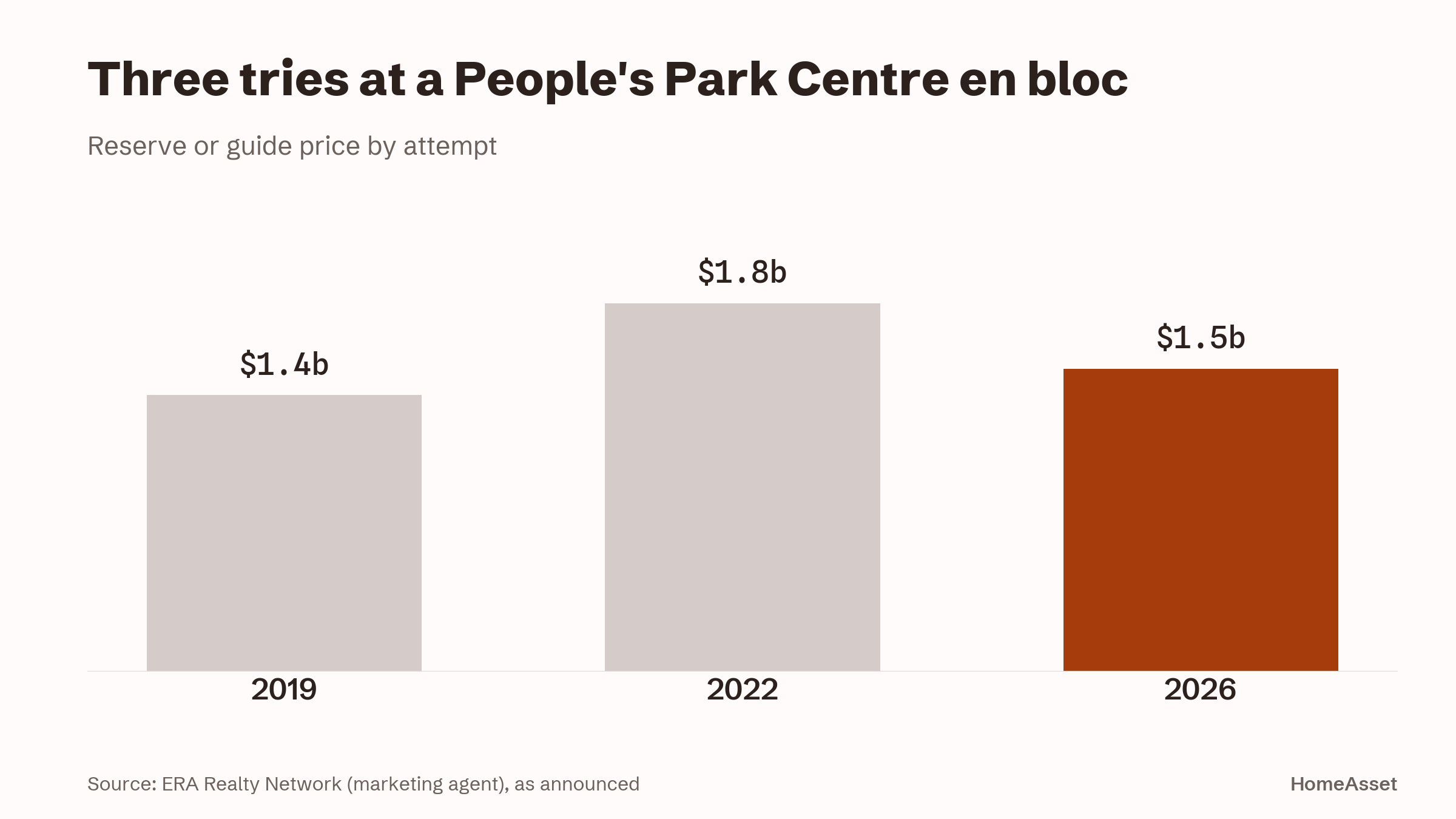

This is a story of a price finding its level. The first attempt in 2019 carried a $1.35 billion reserve but never got to market properly, falling short of the 80% consent. The 2022 attempt went out at a much higher $1.8 billion reserve and closed without a successful bid. The new $1.48 billion guide translates to roughly $2,455 psf per plot ratio, and assumes approval for a lease top-up to a fresh 99 years. Whether a Land Betterment Charge (the tax on the uplift in land value when use is intensified or changed) applies on redevelopment is not yet known.

Third time, lower price: the 2026 guide sits $320 million below the 2022 reserve. Source: ERA Realty Network (marketing agent), as announced.

Third time, lower price: the 2026 guide sits $320 million below the 2022 reserve. Source: ERA Realty Network (marketing agent), as announced.

What a buyer would be getting

The site’s fundamentals are hard to fault. It sits at the junction of Eu Tong Sen Street and Upper Cross Street with a 124m street frontage, connects to Chinatown MRT interchange on the North East and Downtown lines, and is minutes from the CBD. Under the Master Plan it is zoned Commercial with a gross plot ratio of 8.6, making it one of the largest redevelopment opportunities in the Core Central Region. The tender announcement floats a possible mixed-use scheme of around 60% commercial and 40% residential, subject to planning approvals.

The area’s trajectory helps too. The government’s planned 60-storey BTO project at nearby Pearl’s Hill will bring thousands of residents back into the city centre over the coming years, and residents, unlike office workers, generate all-day footfall for shops and food outlets. That plays directly to a mixed-use redevelopment.

Why it is still a hard sell

Scale cuts both ways. A buyer is committing close to $1.5 billion before construction, on a project whose residential units must be sold within five years to qualify for remission of the Additional Buyer’s Stamp Duty (ABSD is the extra stamp duty on residential purchases; developers pay 35% upfront and get it back only if they finish selling in time). On the guide price alone, the sum at risk is roughly $518 million.

There is also the buyer-pool question. Singapore’s largest group of private-home buyers are HDB upgraders, who are mostly families, and Chinatown is short on the schools, parks and larger homes families rank first. With foreigners now paying 60% ABSD, developers cannot count on international buyers to absorb a big CCR project either. Any redevelopment would have to be priced and designed for locals, which is exactly the discipline that the lower guide price reflects.

The pool of developers able to write a cheque this size is small, and recent GLS results show where their conviction currently sits: in large, MRT-linked suburban and city-fringe sites. Still, a landmark CCR plot with an 8.6 plot ratio does not come along often, and the more realistic ask gives this attempt a better footing than 2022’s.

What this means for you

- If you own a unit in an ageing mixed-use complex, note the pattern: consent thresholds and pricing discipline decide whether an en bloc flies. A lower, realistic reserve is what gets tenders moving in this market.

- For buyers watching the CCR, a successful sale here would eventually add a major mixed-use project above Chinatown MRT, but that is years away. Nothing changes for the area’s supply picture in the near term.

- The 60% foreigner ABSD and the five-year sell-out clock keep shaping what developers will pay for big central sites. Expect future CCR launches to be designed around local budgets and family-sized demand, not foreign capital.

- Businesses renting in People’s Park Centre should watch the 16 September tender close. A sale would start a long clock (approvals, then vacant possession), but relocation planning is easier started early.

Sources

Market commentary dated 16 July 2026. Conditions change; verify figures against the primary sources above before acting. This is general information, not financial advice.