New home sales hit a 28-month low in June. Here's the real story

![]() By Alvin Ang

By Alvin Ang

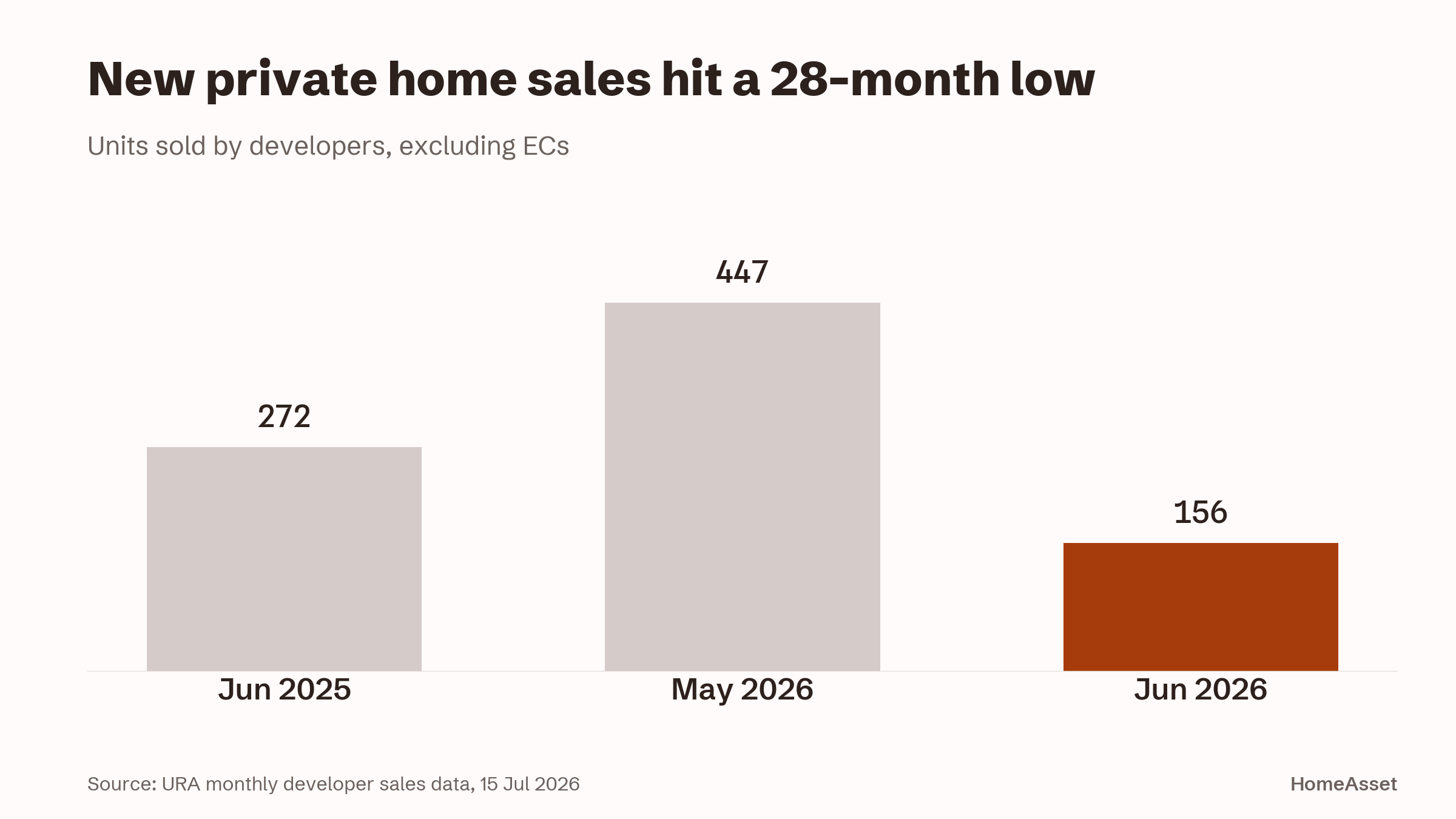

Developers sold just 156 new private homes in June 2026, the lowest monthly tally since February 2024. Before reading that as a market turn, look at the cause: for the first time since URA began publishing developer sales data in 2007, not a single new project was launched in the month.

The June figure, which excludes Executive Condominiums, is a 65.1% drop from the 447 units developers moved in May 2026, and 42.6% below the 272 units sold in June 2025. It is the quietest month in the primary market since February 2024’s 153 units.

June’s 156 units are down 65% from May and 43% from a year ago. Source: URA monthly developer sales data, 15 Jul 2026.

June’s 156 units are down 65% from May and 43% from a year ago. Source: URA monthly developer sales data, 15 Jul 2026.

Why the number collapsed

Two things happened at once. Developers released zero new units for sale, a first in the data’s history, and the near month-long June school holidays pulled buyers and agents overseas. Christine Sun, chief researcher and strategist at Realion Group, noted that developers routinely scale back launches during the June holidays, so a lull was expected even before the zero-launch month made it starker.

Nicholas Mak, chief research officer at Mogul.sg, added a supply-side point: recent launches have sold so well on debut that developers’ unsold inventories have thinned out. With fewer choice units left in earlier projects, there was simply less on the shelf for June’s buyers.

With nothing new to see, buyers went to existing projects, mostly in the city fringe. Based on data compiled by ERA, the Rest of Central Region took 53.8% of June’s sales (84 units), the suburban Outside Central Region 36.5% (57 units), and the Core Central Region 9.6% (15 units).

Hudson Place Residences led the month with 12 units at a median $2,577 psf, with eight of those transacting below $2.5 million, a recurring sweet spot for new private home buyers. The Continuum and Union Square Residences each sold 11 units (median $2,789 psf and $2,762 psf), as did Chuan Park in the OCR (median $2,631 psf).

The half-year tells a different story

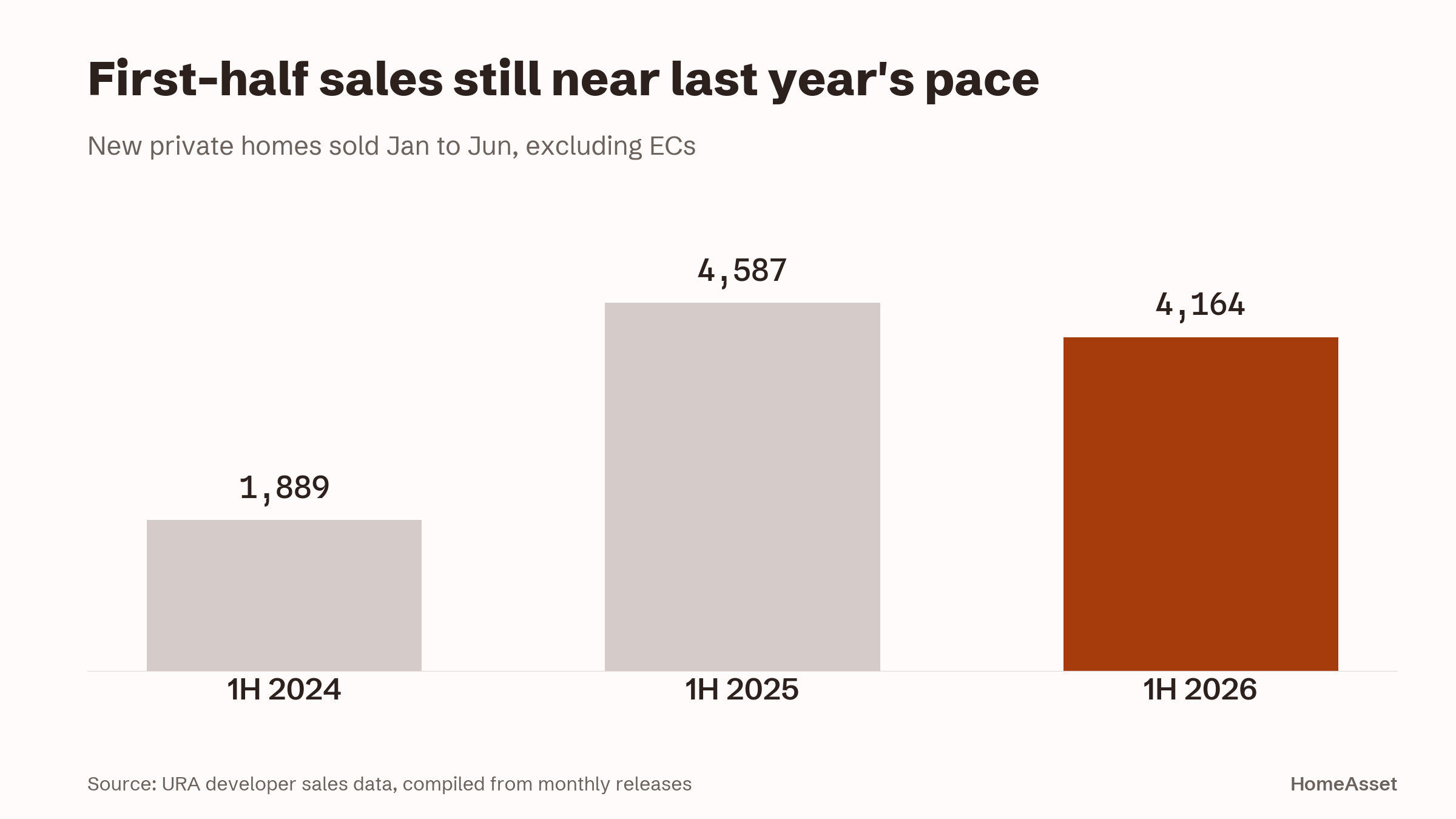

Zoom out and the market looks nothing like a slump. Developers sold 4,164 new private homes in the first half of 2026, more than double the 1,889 units of 1H 2024 and only 9.2% below the 4,587 units of 1H 2025. The gap versus last year largely reflects fewer launches in 1H 2026, not weaker appetite. March and April sales were strong on the back of high-profile launches such as Pinery Residences, Rivelle, Tengah Garden Residences and Vela Bay, even with the US-Iran conflict breaking out in February.

The half-year picture: 2026 is running close to 2025, and far above 2024. Source: URA developer sales data, compiled from monthly releases.

The half-year picture: 2026 is running close to 2025, and far above 2024. Source: URA developer sales data, compiled from monthly releases.

Two pockets stayed firm through the quiet month. New landed home sales held at six units, matching March and April, driven mainly by Pollen Collection II, according to Mohan Sandrasegeran, head of research and data analytics at SRI. And high-value deals kept climbing: 60 new CCR non-landed homes sold for between $5 million and $10 million in 1H 2026, up 185.7% from 21 such deals in 1H 2025, as Singapore’s safe-haven status keeps drawing wealthy buyers to prime assets.

July launches already point to a rebound in volumes as new projects hit the market.

What this means for you

- Do not read June as a price signal. Sales fell because nothing launched, not because buyers walked away. Underlying demand showed up wherever stock existed.

- If you are waiting for launch-month discounts, this data argues against it: thin unsold inventory means developers are under little pressure to cut prices.

- The sub-$2.5 million quantum keeps proving to be the crowd’s sweet spot. If that is your budget, expect the most competition for exactly those units at July’s launches.

- City-fringe (RCR) projects are absorbing most of the demand between launches. If you are comparing resale versus new in the RCR, note that new-launch medians there are sitting around $2,600 to $2,800 psf.

Sources

- URA monthly developer sales data (Property Market Information)

- Realion Group (Christine Sun, Chief Researcher & Strategist), paraphrased

- ERA Singapore, sales data compilation, paraphrased

- Mogul.sg (Nicholas Mak, chief research officer), paraphrased

- SRI (Mohan Sandrasegeran, Head of Research & Data Analytics), paraphrased

Market commentary dated 16 July 2026. Conditions change; verify figures against the primary sources above before acting. This is general information, not financial advice.