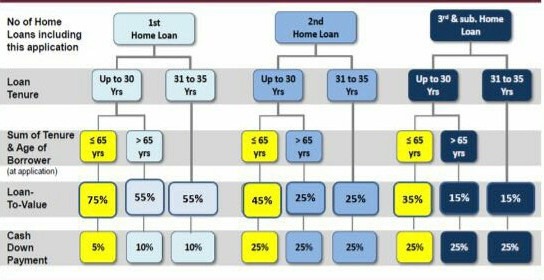

Understanding Housing Loan Limits in Singapore: A Guide to Loan-to-Value (LTV) Ratios

Navigating the world of housing loans in Singapore can be complex, especially with evolving regulations on loan-to-value (LTV) ratios and down payment requirements. For both new and experienced homeowners, it’s essential to understand how these rules affect your ability to borrow and invest in property. At HomeAsset.sg, we break down the current LTV limits, down payment requirements, and key factors affecting Singapore housing loans, all illustrated in the helpful chart below.

Billy The Editorial Guy

10/26/20244 min read

What is Loan-to-Value (LTV) Ratio?

The Loan-to-Value (LTV) ratio is the maximum percentage of a property's value that banks are allowed to lend to home buyers. The LTV ratio impacts the loan amount you’re eligible for and the minimum down payment required. In Singapore, LTV ratios vary based on factors like the number of home loans you already hold, the loan tenure, and your age.

To make it easier, here’s a breakdown of the LTV ratios based on the number of existing loans, loan tenure, and borrower age, as illustrated in the chart below.

Key Takeaways from Singapore’s Loan-to-Value Ratio Regulations

1. For First-Time Home Buyers

LTV Limit: Up to 75% if the loan tenure is within 30 years and the borrower’s age plus loan tenure does not exceed 65 years. This means first-time homebuyers need a 25% down payment, with at least 5% in cash.

Longer Tenures or Older Age: If the loan tenure is between 31 and 35 years, or if the sum of the borrower’s age and loan tenure exceeds 65 years, the LTV cap is reduced to 55%, increasing the required down payment.

Example: If you’re 40 years old and want a loan tenure of 35 years, the sum (40 + 35) equals 75, which means you’ll only qualify for an LTV of 55%.

2. For Second Home Loans

LTV Limit: For borrowers with an existing housing loan, the maximum LTV drops to 45% if the loan tenure is up to 30 years and the borrower’s age plus loan tenure is 65 years or below. This translates to a 55% down payment requirement, with at least 25% in cash.

Stricter Terms for Extended Loans: If the loan tenure exceeds 30 years or the borrower’s age and loan tenure exceed 65 years, the LTV is further reduced to 25%, requiring a significant 75% down payment.

Example: For a 45-year-old with an existing loan, applying for a 35-year loan means the LTV cap will be 25%, and 75% of the property value must come from down payment funds.

3. For Third and Subsequent Home Loans

LTV Limit: For borrowers with two or more existing home loans, the LTV cap is reduced further to 35% for loan tenures up to 30 years and if the borrower’s age plus tenure does not exceed 65 years.

Minimum Down Payment: Borrowers in this category must be prepared with a cash down payment of at least 25%.

Additional Restrictions: If the loan tenure is over 30 years or if the borrower’s age plus loan tenure exceeds 65 years, the LTV cap drops to just 15%, meaning buyers must put down 85% of the property value.

Example: A 50-year-old purchasing a third property with a 35-year loan will be subject to the lowest LTV limit of 15%, meaning they need an 85% down payment.

How Does Loan Tenure and Age Impact Your Loan Eligibility?

As shown in the table above, both loan tenure and the borrower’s age play a crucial role in determining the LTV cap. Here’s how these factors affect your borrowing power:

Shorter Loan Tenures (Up to 30 Years): These tenures allow for higher LTV limits, as shorter loan durations reduce the bank’s risk. Younger borrowers with shorter tenures generally qualify for higher LTVs.

Longer Loan Tenures (31 to 35 Years): Extending the loan tenure often results in a reduced LTV ratio, requiring a larger down payment. This is particularly important for older borrowers, as higher ages combined with longer tenures lower the allowable LTV.

Age and Loan Tenure Combined: When the sum of your age and loan tenure exceeds 65 years, expect a reduced LTV cap, even for first-time homebuyers. This rule is in place to ensure that borrowers remain capable of repaying their loans as they approach retirement age.

Cash Down Payment Requirements

In addition to LTV limits, Singaporean regulations mandate specific minimum cash down payments based on the number of loans:

5% for First-Time Buyers: If you’re taking your first housing loan, a minimum of 5% cash is required as part of the total 25% down payment.

25% for Multiple Loans: For second or subsequent housing loans, the minimum cash down payment increases to 25% of the property’s purchase price or valuation, whichever is lower.

This cash component cannot be financed through CPF or any other loan, making it essential for borrowers to prepare liquid funds for property purchases.

Maximizing Your Housing Loan Potential in Singapore

Navigating LTV limits and TDSR requirements can be complex, especially when multiple factors like age, tenure, and existing loans come into play. Here are some tips to maximize your borrowing potential:

Pay Down Existing Debts: Reducing outstanding debt can improve your TDSR, which is essential for borrowers with higher loan needs.

Choose the Right Loan Tenure: A shorter loan tenure can improve LTV eligibility but comes with higher monthly payments. Plan based on your long-term financial stability.

Prepare Adequate Cash Reserves: Given the high cash down payment requirements for second and third loans, saving in advance ensures you meet down payment obligations without financial strain.

Monitor CPF Usage: CPF savings can be utilized for down payments, but only up to the non-cash portion. Ensure that you balance CPF usage for property with future retirement needs.

Conclusion

Understanding LTV limits, cash down payment requirements, and the effects of loan tenure and borrower age are essential for anyone looking to purchase property in Singapore. With stricter guidelines from MAS, first-time buyers and investors must approach property financing with careful planning. Whether you’re buying your first home or expanding your portfolio, these insights can help you make informed decisions.

At HomeAsset.sg, we provide up-to-date information and expert advice on Singapore’s property market. Visit our blog for more insights and resources to navigate the complexities of housing loans in Singapore.