Decoding Your Credit Report: What Singapore Borrowers Need to Know

Understanding your credit report is essential for managing your financial health, especially in Singapore, where creditworthiness plays a crucial role in securing loans and achieving financial milestones. But credit reports can often seem complex, with multiple categories, scores, and statuses. In this guide, we’ll break down each section of your credit report, so you know exactly what lenders see and how to interpret your financial standing.

Billy The Editorial Guy

10/28/20245 min read

What is a Credit Report, and Why Does It Matter?

A credit report is a comprehensive record of your credit history and financial behavior, compiled by the Credit Bureau Singapore (CBS) with data from major financial institutions. It reflects your borrowing habits, payment history, and current debt obligations, giving lenders a snapshot of your creditworthiness. Banks, financial institutions, and other lenders use this report to assess risk when deciding whether to approve your applications for loans, credit cards, or other financing options.

By understanding your credit report, you can take proactive steps to improve your credit score, identify potential errors, and address any red flags that might impact your loan eligibility.

Key Components of a Singapore Credit Report

Your credit report contains various sections that provide different insights into your financial history. Let’s break down each part.

Image from Credit Bureau Singapore

Image from Credit Counselling Singapore

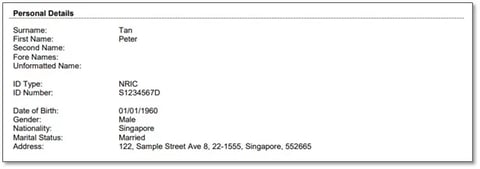

1. Personal Details and Identification

This section contains your basic personal details—such as your name, NRIC, and additional identification markers. It’s primarily used for verification purposes to ensure that your credit data is accurate and assigned to the correct individual.

Tip: Regularly check that your details are up-to-date, as inaccuracies here could affect your report access or create confusion for lenders.

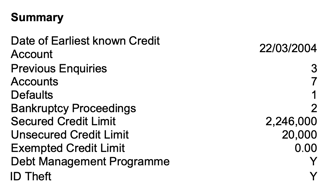

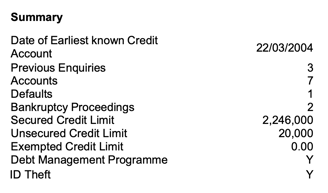

2. Summary of Credit Information

The summary section offers a quick overview, including:

Total Credit Limits: Your combined credit limit across various secured, unsecured, and exempted credit facilities.

Debt Management and Identity Theft Flags: Indicators that highlight if you’re enrolled in a debt management program or if there’s any record of identity theft.

Why it Matters: This snapshot provides lenders with a quick assessment of your credit profile, making it essential for you to ensure it reflects your current financial situation accurately.

3. Account Status History

The account status history provides a rolling 12-month record of your credit accounts. Each month’s status is marked with specific symbols that reflect the payment behavior for each account:

A: Payments current or less than 30 days overdue.

B: Payments 30-59 days overdue.

C: Payments 60-89 days overdue.

D: Payments 90 days or more overdue.

Additional codes indicate closed accounts, default statuses, or restructured loans.

This section also indicates cash advances, balance transfers, and whether full payments were made on credit card accounts.

Understanding Symbols: These codes provide a transparent view of your payment history and reliability. Any overdue status could negatively impact your credit score, while consistent “A” statuses show timely payments.

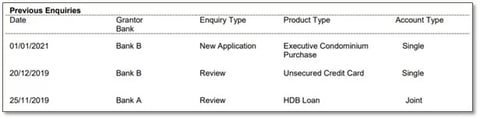

4. Previous Enquiries

This part lists all inquiries made on your credit report by lenders over the past two years. Each inquiry represents a loan or credit application, which may affect your credit score if done frequently.

Tip: Avoid multiple credit applications within a short period. Too many inquiries can signal financial distress to lenders and negatively impact your credit score.

Image from Credit Counselling Singapore

Image from Credit Counselling Singapore

Image from Credit Counselling Singapore

Image from Credit Counselling Singapore

5. Default Records and Repayment Statuses

Default records display any instances where payment obligations were not met, as reported by your lenders. These are categorized as:

Outstanding: The default remains unpaid.

Negotiated Settlement or Full Settlement: The debt has been resolved through partial or full payment.

Defaults with statuses like "Outstanding" remain on the report indefinitely, while settled defaults are displayed for up to three years.

Impact on Your Score: Defaults are a significant red flag for lenders. Settling defaults, even partially, can help in improving your credit profile over time.

Image from Credit Counselling Singapore

6. Debt Repayment Scheme (DRS) Records

This section lists any participation in Singapore's Debt Repayment Scheme (DRS), managed by the Insolvency and Public Trustee Office (IPTO). Each status—such as “Under Assessment,” “In Progress,” or “Bankrupt”—reflects the borrower’s current position in the repayment process.

Why It’s Important: DRS records show lenders your commitment to addressing debt issues. Even if you’ve struggled financially, actively participating in repayment programs can reflect positively on your report.

Image from Credit Counselling Singapore

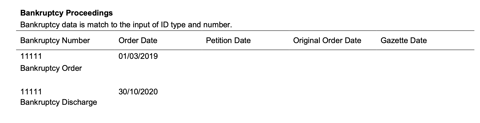

7. Bankruptcy Proceedings

If you’ve been involved in bankruptcy proceedings, those details will be available here and remain on your credit report for five years after discharge. This is consistent with the retention period set by IPTO.

What You Should Know: Bankruptcy records have a significant impact on creditworthiness. However, upon successful discharge, borrowers can gradually rebuild their credit profiles over time.

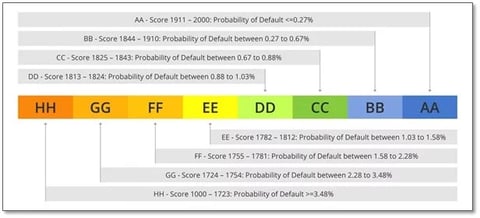

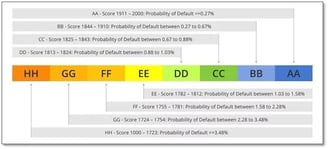

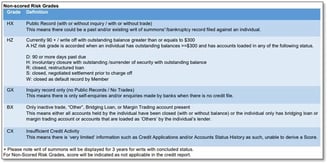

8. Credit Bureau Score

The Credit Bureau Score (CBS Score) is a numeric representation of your credit risk, calculated using your credit data. The score ranges from 1000 to 2000, with the following risk grades:

AA (1911–2000): Lowest risk of default.

BB to CC: Moderate risk, indicating some payment issues.

HH (1000–1723): High risk, with a default probability over 3.48%.

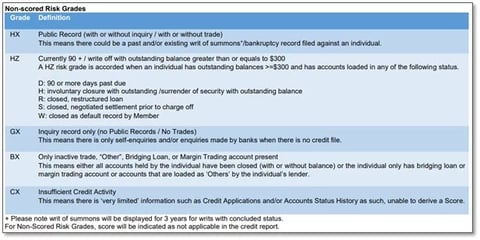

Certain non-scored risk grades, like HX (public records) and HZ (90+ days overdue or write-offs), denote significant issues without assigning a score.

Boosting Your Score: Timely payments, reducing outstanding balances, and avoiding defaults are key to maintaining a high credit score. It’s also important to keep your debt levels manageable to prevent a low CBS Score.

Image from Credit BUREAU Singapore

Image from Credit BUREAU Singapore

Image from Credit BUREAU Singapore

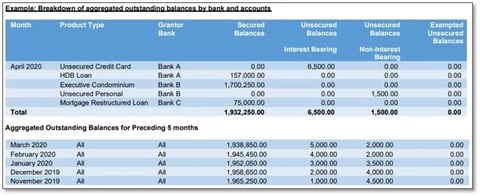

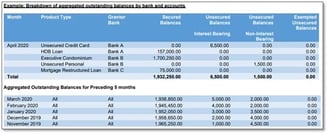

9. Aggregate Outstanding Balances

This section details the total outstanding balances across different credit products. It categorizes balances as secured or unsecured, and highlights interest-bearing and non-interest-bearing debts.

Quick Insight: Lenders use this overview to evaluate your total debt exposure. Managing these balances well—especially by reducing high-interest debt—improves your credit profile and enhances borrowing potential.

Key Takeaways for Managing Your Credit Report in Singapore

Maintain a Clean Payment History: Ensure timely payments on all accounts to avoid overdue statuses in your account history. These records heavily influence your score and loan eligibility.

Limit New Credit Enquiries: Frequent credit applications can negatively affect your report. Make inquiries strategically to keep your score in good standing.

Address Defaults Promptly: If defaults occur, work towards a settlement. Even a partial payment status is more favorable than an outstanding default on your report.

Stay Informed About Your Score: Your CBS Score reflects your overall creditworthiness. Regularly reviewing it helps you monitor progress and adjust financial habits as needed.

Utilize Debt Management Programs if Necessary: Programs like the DRS are available for those facing financial difficulties. Enrolling in such schemes demonstrates responsibility and commitment to repayment.

Conclusion: Take Control of Your Financial Health

Your credit report is more than a collection of financial data—it’s a vital tool for understanding and managing your financial health. By monitoring your report and maintaining good credit habits, you can enhance your loan eligibility, secure favorable terms, and achieve financial goals. Visit HomeAsset.sg for more insights and guidance on financial health, loans, and credit management in Singapore. View the full explainer from Credit Bureau Singapore here